loan

Settle Unpaid Loans With Debt Consolidation in the Philippines

It is essential that you handle your debts properly in order to build a good credit score as an individual who is financially responsible. Nevertheless, some people are unable to pay back their unpaid loans because their salary and financial capacity aren’t proportional to the amount they borrowed.

Nevertheless, you can make loan repayments more manageable and efficient with one solution: debt consolidation.

What is Debt Consolidation?

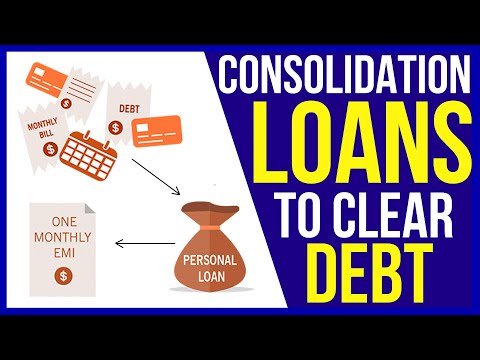

Consolidating debt[1] involves bringing together multiple debts and turning them into one payment. The debt consolidation process can be carried out in two ways: by taking out a debt consolidation loan or by transferring credit card debt to another credit card.

How Debt Consolidation Works in the Philippines

You can think of it as putting Debt #1, Debt #2, and Debt #3 in one box. In that case, the three debts will be converted into a single loan.

Invoices issued by the box will state a fixed amount that you must pay each month. As long as you pay that fixed amount monthly, you’re actually paying off the three debts you’ve placed inside that box.

When is Debt Consolidation a Good Idea?

Consolidating Debt has two obvious advantages, both of which are obvious. In the first place, it can be viewed as a practical method of stopping high interest payments on existing debts. As a second benefit, it allows you to organize your debts in a manageable manner.

When You’re Dealing with High Interest Rates

You should consider debt consolidation if you have high-interest debts, such as credit card bills. With a new loan that has a lower interest rate, you will be able to pay down or pay off all your debt easier. Additionally, the payment schemes are manageable, albeit much longer.

When You Want to Organize Your Debts

You can also use it if you want to organize a manageable amount of debt. The due dates of a number of debts are usually different, making it difficult to make monthly payments. But,Consolidating your debts into one payment allows you to remember just one due date. Setting aside repayment money and automating your monthly payments will be easier.

When You Want to Clear Your Debts Fast

Debt consolidation loans have the advantage of helping you pay your debt faster since you follow a payment schedule. You can apply for a debt consolidation loan with a maximum repayment period of 12 months if you want to settle your debts within a year.

Debt consolidation can also help you pay off significant debt faster. You don’t have a timeline with credit card providers to pay off your balance, but you do with debt consolidation loans.

When You Need More Time to Pay Off Your Loans

The opposite of the preceding benefit. Debt consolidation loans with a longer term may be a better option if you have cash flow problems. As a result, your debt will have more time to be settled. On the other hand, paying more interest over time is a downside.

When You Have a Good Credit Score for Leverage

You can apply for a loan that has a lower interest rate if you have a good credit score. This will result in you saving on interest over the course of your chosen loan term.

When is Debt Consolidation a Bad Move?

Consolidating debt has both pros and cons. However, the drawbacks aren’t usually taken into consideration. Here are some situations where debt consolidation isn’t practical:

When You Think it Will Eliminate All Your Debts

Consolidating your debt becomes a disadvantage when you think it will magically resolve all your debts. Combined payments allow you to feel free of debt because your debts are consolidated. Your dangerous thinking may lead you to get another loan.

When Fees are a Burden

Loan consolidation usually comes with fees. You may need to pay balance transfer fees when you transfer debt from one credit card to another. Also, you may need to cover closing costs and annual fees.

Debt consolidation loans, which are technically new loans, are not guaranteed to have lower interest rates. You will still need to check with your lender and your credit score. There is even a possibility that your monthly payments will be higher.

Your debt consolidation loan term will likely be extended if you pay less every month. This also means extending the interest payment period. Long-term, you may pay more interest.

You should avoid debt consolidation loans if you are also prone to missing payments. As the late payment fees mount, you’ll owe a lot more.

When Your Debt is Small and Manageable

Consolidating debts usually works for larger debts. When you have a single debt that you can pay within five to six months, you probably don’t need it. Your credit card may even offer zero-interest purchases.

To avoid penalties, just remember your due dates.

Does Debt Consolidation Hurt Your Credit Score?

Depending on the situation. Your credit score can improve if you are a diligent payer. With only one due date to remember, you can easily set aside money or automate payments, ensuring on-time payments. Making your payments on time is one way to improve your credit score.

However, consolidating your debts can also harm your credit score. A new credit card’s limit may get maxed out if you transfer all three of your other credit cards’ debts to it.

Creditors should be wary of this. The result might be a decrease in your credit score.

Who is Eligible for a Debt Consolidation Loan?

It is possible to consolidate debt with a personal loan. Therefore, the usual requirements apply. According to your lender, you must meet the following requirements:

-

Ages 21 to 65 are required.

-

If you are a foreigner, you must be a Filipino resident.

-

Principal credit card holder (some lenders do not require this).

-

It is necessary for you to meet the minimum income requirement (some lenders require at least $15,000 per month while others require at least $20,000).

14 Debt Consolidation Loans in the Philippines

The two ways to consolidate your debts are through a debt consolidation loan and by transferring your credit card debt to another card.

In contrast, debt consolidation loans may seem foreign and technical to many people, while the second method is fairly straightforward to grasp.

Personal loans can be used for debt consolidation. Loan consolidation is available from a number of lenders in the Philippines. Personal loans for debt consolidation are not available at all banks and lending companies.

Philippines debt consolidation loans include:

UnionBank Personal Loan

Key features:

-

Amount of loan: Up to $2 million

-

Add-on rate: 1.29% per month

-

A one- to five-year loan is available

-

Time to approve: Within five minutes

With UnionBank’s personal loan for debt consolidation, you can borrow up to ₱2 million with flexible repayment terms of up to five years. A UnionBank debt consolidation loan does not require collateral.

The annual contractual interest rate is 26.9%, which is a relatively low rate. There are also charges for disbursement and closing.

Your loan can be disbursed as soon as 24 hours after approval.

Approval Requirements

Debt consolidation loans in the Philippines require a good credit report, a good payment history, and a stable income. Shortly, there shouldn’t be any red flags that indicate you’re a big risk.

Look for other debt consolidation loans in the Philippines with easier requirements or more flexible approval criteria if you have a less-than-stellar credit report due to unpaid loans or credit cards.

You can also get a secured loan if you need a large loan amount and have an eligible asset, such as a house or car, to pledge as collateral.

Fees and Interest Rates

Philippines debt consolidation loans often advertise low interest rates, but these aren’t always guaranteed. Credit still determines the actual rate. Take into account origination fees, late fees, and prepayment penalties as well.

Compare quotes from different lenders. To determine your interest rate, compare and then fully understand the terms and conditions.

Loan Amount

Having a large amount of debt to consolidate will require a larger loan amount. Research debt consolidation lenders to find one that offers the amount you need.

Loan Terms

Consolidate your debt with a lender who offers terms you can afford.

In particular, if you’re working within a limited budget, a longer term may be the best choice for you. Because the monthly payments are usually low, this is the case. In the end, this may mean paying more interest than you’d like.

Choose a loan term that is as short as possible. Despite the high monthly payment, your debts will be paid off quickly.

Application Process

When considering an application, take into account its ease of use, especially if you are a busy individual. Many lenders now allow borrowers to apply online. When you work with a provider of loan consolidation in the Philippines, you will save time.

Customer Service

Consolidation loans should provide several customer service options. Ensure that the debt consolidation loan provider offers customer service facilities such as chat, email, and 24-hour hotlines before applying.

Alternatives to Debt Consolidation Loans in the Philippines

Consolidating debt is not always the best solution. Alternatively, you can try:

Adjust Your Budget and Financial Habits

It may be possible to tweak your budget a little bit if your running debts are still manageable. When you can, reduce your monthly expenses (e.g., cook your own meals instead of eating out, save electricity, buy generic products instead of branded ones, etc.). Using the savings, you can pay off your debt.

Get Refinancing

A refinance involves taking out a new loan to settle an outstanding debt. In this strategy, you take advantage of low interest rates.

The refinancing of a home loan is a common method of repaying it. The program, however, does come with some fees.

Apply for the Credit Card Amnesty Program in the Philippines

A credit card amnesty program, also called the Interbank Debt Relief Program (IDRP), restructures your debt by rolling it together with a repayment plan. Through low interest rates and affordable monthly amortizations, it makes repayment easy.

IDRP interest rates can reach up to 1.5%. Tenors of up to 10 years are possible, but they are usually reserved for extreme situations.

The Bangko Sentral ng Pilipinas (BSP) manages this program, along with member banks of the Credit Card Association of the Philippines (CCAP).

FAQs

QNO(1):Debt Consolidation Options in the Philippines

Ans:Debt Consolidation Loans – Personal loans come with fixed interest rates and terms, making budgeting easier. There are also many of them online, and some of them even offer loan apps (like my own).

QNO(2):Will banks do debt consolidation loans?

Debt consolidation loans are available from banks, credit unions, and installment loan lenders. A consolidation loan simplifies how many payments you have to make by consolidating several debts into one. There is also the possibility that these offers will be for lower interest rates than what you are currently paying.

Conclusion

Debt Consolidation can be a practical solution for managing and repaying multiple debts efficiently, particularly when dealing with high-interest rates or a desire for better organization. However, careful consideration of individual financial circumstances and alternative strategies, such as budget adjustments and refinancing, is essential to make informed decisions.